TQ Morning Briefing

TSMC delivered the print the market asked for. Asian chipmakers sold off anyway. Korea just hiked rates for the first time since 2023.

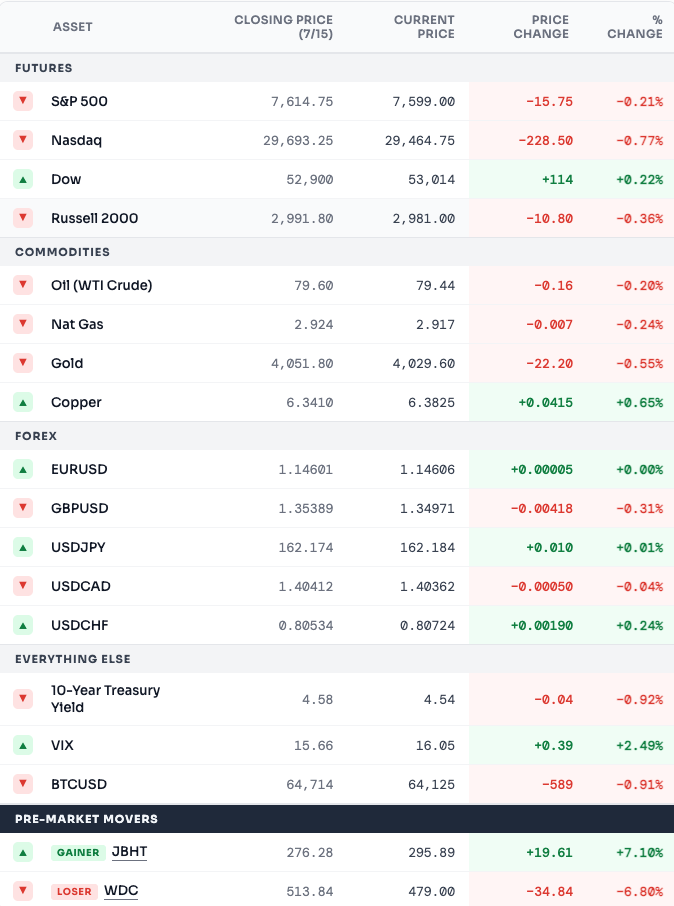

Two cool price level prints this week.

The July hike debate has been effectively settled. But futures point lower this morning anyway.

The reason is Asia.

TSMC (TSM) posted record profit and revenue at the top of guidance overnight. The ADR barely moved in pre-market. Taiwan's Taiex closed lower. Samsung fell sharply. SK Hynix fell further. Korea's KOSPI had one of its worst sessions in years. Japan's Nikkei followed.

The demand story was confirmed. The equity story is being repriced anyway.

The dollar is flat in most crosses. It firmed against the won ahead of the Bank of Korea decision. Oil slightly lower despite fresh Iran-US strikes overnight. Gold continues to lag.

Market Implication

The macro tape says slower growth and a Fed pinned on hold. The earnings tape says AI hardware is being re-rated no matter the print. Watch the semi ETF into the open. If it holds on a top-of-guidance TSMC print, the re-rating is done. If it fades, the pipeline has more to work through.

The Multi-Billion Dollar Scam Nobody's Talking About

Fraud is being exposed everywhere right now. Billions gone.

But they're missing the big one...

A legal scam that affects 95% of ALL Americans.

Oxford Club's own Marc Lichtenfeld hit the streets of South Florida to expose it in broad daylight.

Watch along as he captures real people's reactions LIVE on camera.

Two mechanisms.

Demand accelerated. Multiples compressed. TSMC guided the quarter high. It delivered at the top of that guide. Margins printed above the top of range. High-performance computing now dominates the mix. Order books are the leading indicator. Multiples are the lagging one. The two just moved in opposite directions in the same session. That is a re-rating in real time.

Central banks are diverging again. Korea just hiked. It is the first Bank of Korea hike in more than three years. Won weakness and imported inflation from the Iran war forced it. The Fed sits on hold with cooler CPI and PPI both landing this week. Asian rate paths are turning up while the US sits pinned on hold. Dollar-Asia FX shows it first.

Structural Setup

Confirmed demand meets compressing multiples. TSMC is the cleanest read. The chip designers report in August. If they rally into their prints despite the drag today, the re-rating stops at foundry. If they lag their own strong numbers the way TSMC just did, it spreads.

Yesterday's US session held on two legs.

Money-center banks reported strong quarters and were bid. Megacap tech carried the tape into the close. The chip complex bled underneath both. That rotation did not stop at the US close. It rolled straight into Asia.

ASML (ASML) closed lower yesterday despite raising guidance again. Samsung and SK Hynix took the worst of the Asian session. The KOSPI dropped hard. It was the worst developed-market session in months. Taiwan Taiex held better but still closed lower on the TSMC print.

The mix that led yesterday is not rotating. Banks are bid on the strong Tuesday and Wednesday prints. Megacap tech holds. The rotation is out of AI hardware. This is a narrowing, not a broadening.

Sector Read

Watch the semi ETF against the Nasdaq. If chips underperform into the close while the index holds, the re-rating stays narrow. If the Nasdaq slides with chips, the AI trade broadens into its consumers. Nvidia (NVDA) sits at that transmission.

15X Bigger Than SpaceX: Elon's New Launch

While the rest of the market goes crazy for "the mother of all IPOs", a new Elon Musk innovation is quietly being rolled out nationwide. It's been 27 years in the making, and it could have a radical impact on how millions of people manage their money… and even collect Social Security. Here's everything you need to know.

This ad is sent on behalf of InvestorPlace Media at 1125 N. Charles Street, Baltimore, Maryland 21201. If you're not interested in this opportunity, please click here.

Korea did something no other major central bank has done since the Iran war started.

It hiked to defend the currency and offset imported inflation. This is the first evidence the war is transmitting into monetary policy in Asia. Not just oil prices.

Indonesia, the Philippines, and India are next if oil holds. That would be the first synchronized Asian tightening cycle in years.

The Fed sits on the other side. The July 29th meeting is under two weeks out. Warsh spent two days telling Congress the committee has no tolerance for high inflation, but told the Senate yesterday that AI-driven price increases are not structurally inflationary because a supply response will follow. Korea just hiked on the same imported inflation Warsh called transitory. Two central banks. Same inflation source. Opposite responses. Traders now price July as a near-certain hold. September sits between hold and hike.

Watch Signal

Watch the won. If it firms after the hike, the market bought the defense. If it weakens further, the Asian FX complex is next. Thai baht and Indian rupee read it first.

UnitedHealth (UNH) reports before the open.

Yesterday Elevance Health (ELV) fell sharply. It will exit several Medicaid markets over the coming quarters. The managed care sector sold off with it. Now the sector's biggest name reports. Same question the market just asked Elevance.

Is Medicaid a company problem or a sector problem?

If UnitedHealth cuts guidance on managed care mix, the answer is sector. The complex re-rates the way chips are re-rating now. Centene and Molina report next into a lower bar. If UnitedHealth holds the guide and points to enrollment strength, the answer is company. Elevance carries the discount alone.

The Read

Medicaid margins are the mechanism. The pressure came in fast enough that Elevance chose exit over adjustment. UnitedHealth has more scale to absorb it. If its guide moves modestly lower, Centene walks into a coiled spring.

Navellier Warns: This Could Leapfrog Elon's SpaceX IPO

Elon Musk could take SpaceX public in 2026, at an estimated $1.75 trillion valuation. The IPO would include Elon's AI model, Grok. But according to Louis Navellier, a radical new AI model will launch this year… over 1,000 times more powerful than Elon's. And the company behind it could outperform SpaceX in the process.

Click here for full details (including Louis' new pick — free).

This ad is sent on behalf of InvestorPlace Media at 1125 N. Charles Street, Baltimore, Maryland 21201. If you're not interested in this opportunity, please click here.

Economic Data: Retail Sales, Initial Jobless Claims, Philly Fed Manufacturing, Business Inventories, Pending Home Sales, NAHB Housing Market Index

Fed Speakers: Logan at 12:30 PM ET

Earnings: UnitedHealth (UNH), GE Aerospace (GE), Abbott (ABT), US Bancorp (USB), Truist Financial (TFC), State Street (STT), Citizens Financial (CFG), Prologis (PLD), ManpowerGroup (MAN) before open | Netflix (NFLX), Intuitive Surgical (ISRG), Alcoa (AA) after close

Overnight: Nikkei -2.79%, Shanghai Composite -1.85%, FTSE -0.31%, DAX -0.66%

Retail sales lands at eight-thirty.

UnitedHealth reports before that. Logan speaks at twelve-thirty. Netflix (NFLX) reports after the close.

Four tests. One session.

Retail sales ex-autos is expected to flip negative from a strong positive last month. That would be the first monthly drop in the discretionary line in months. If it prints that way, the consumer question rejoins the tape.

UnitedHealth tests whether managed care is Elevance's story or the sector's story.

Logan is the first Fed voice on tape since Warsh finished his testimony. Anything about the July twenty-ninth meeting sits at the front of the price.

Netflix reports into a stock trading near recent lows. Engagement is the debate. Ad growth is the offset.

If retail ex-autos prints negative and UnitedHealth cuts, September hike bets die. If either holds, the July twenty-ninth meeting sits where Warsh left it.

The market walks in wanting one story. It walks out with four data points arguing four different ones.