TQ Morning Briefing

Netflix guided third-quarter growth below what the street wanted. Shares fell sharply after the close. Overnight, Asia sold what remained of the AI trade, with Tokyo leading the drop. The Iran oil waiver ended at midnight. This morning is a repricing, not a headline.

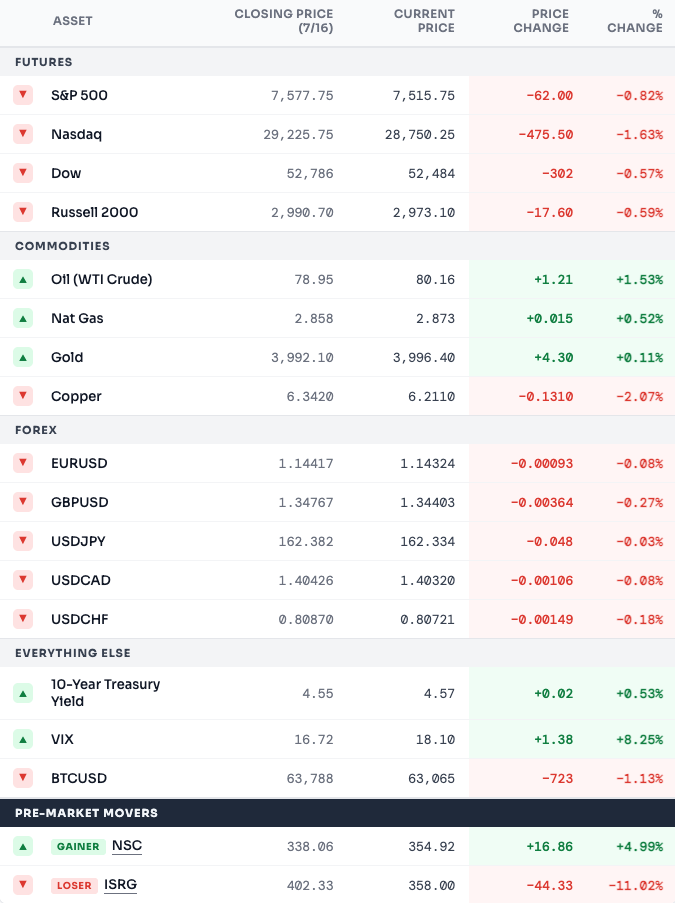

Futures are sharply risk-off ahead of the open.

The Nasdaq is leading the selling. Netflix (NFLX) fell heavily after hours on a soft third-quarter revenue guide. The overnight session made clear this was not a Netflix problem. Tokyo Electron dropped high single digits. SoftBank fell double digits. Advantest took the same treatment. That is Japanese institutional flow at scale.

Bonds are bid. Fed Vice Chair Jefferson said Thursday he would back a rate hike. His condition: inflation stays sticky. That makes the July 29 meeting genuinely two-sided.

The dollar held. The yen did not. Dollar-yen sits near a level Japan has not seen in four decades. Finance Minister Katayama spent the overnight session jawboning. That is the quiet signal under the equity print.

Oil pushed higher. The Treasury's approval for new Iranian oil deals ended overnight. The market had partly priced that in while the waiver held.

Market Implication

The move started in US chips. It went global overnight. Whether Fed centrists follow Jefferson decides if July turns hawkish. That answer arrives in twelve days.

New "AI Fuel" discovered near Grand Canyon

A small drilling crew just punched through to a discovery big enough to meet global electricity demand 140 times over, according to the International Energy Agency...

Right near the Grand Canyon.

See why Google, Berkshire Hathaway and the President of the United States are rushing to grab it >>

Yesterday's read was hedge fund de-grossing. Positioning. Mechanical. Temporary.

Overnight rewrote the story.

Tokyo Electron did not fall high single digits because a hedge fund unwound a short. It fell because Japanese institutional money sold. SoftBank falling double digits is retail plus institutional exiting the country's largest AI proxy. That is a sentiment turn.

The AI hardware trade has shifted from de-grossing to de-rating. Those two look alike over a session. They diverge over a week. See the Asia session damage for the shape of it.

The Iran waiver adds a second layer. Buyers in China, Turkey, and India had a legal window. It closed at midnight. Every cargo now carries secondary sanction risk. The floor under Brent just became a wedge.

Structural Setup

Energy stays bid until a diplomatic path reopens the waiver conversation. Duration stays two-sided until July 29 answers whether Jefferson speaks for the committee. Neither trade resolves cleanly this week. The Iran waiver ending is the specific mechanism that turns Warsh's transitory-inflation framing into Waller's structural-inflation warning. What was a policy debate becomes a data point.

Chip supply chain led the losses in Asia.

It will lead futures at the open. The pain hit equipment and memory hardest. The whole value chain is repricing at once.

The earnings bar has moved.

Yesterday TSMC beat and got sold because it spent too much. Overnight Intuitive Surgical (ISRG) beat on revenue and profit. The stock got sold because guidance was held, not raised. Last quarter the same company beat and raised. The stock popped. This quarter it held. The stock fell hard.

Beat is no longer the bar. Raise is. Every name reporting next week faces a different market template.

Small caps caught a modest bid Thursday while the index bled. That divergence tells you the tape is trying to rotate. Whether the rotation survives a session where futures gap lower is Friday's question.

Sector Read

Watch the equal-weight S&P against the cap-weighted through the open. A stable spread confirms the de-rating is name-specific. A widening spread confirms the AI hardware trade has broken. The rotation has to be paid for.

He predicted the 2008 financial crisis…

He predicted Trump’s election in 2016….

He even predicted the rise of COVID-19 writing:

“The chance we don’t have something on the scale of a national pandemic in the next few years is near zero”

That was three months before the first reported case.

If he’s right again, God Bless America…

Because this crisis will be tectonic in scale…and it's going to begin with the bubble popping in AI.

The US Treasury waiver on new Iranian oil deals ended at midnight.

Buyers who moved barrels legally during the window can no longer. The war entered its sixth night of American strikes overnight. Reports of activity spread beyond the Strait. War-risk premiums for the corridor are rising fast.

Jefferson matters more than his usual centrist framing suggests. Dallas Fed's Logan already floated a hike case. Jefferson is the first centrist to follow. The July 29 meeting was a hold consensus a week ago. It is not now.

The yen tells the third story. Katayama's jawboning is one step short of intervention. If the BOJ hikes to defend the yen, JGB yields rise. Japanese life insurers pull capital home. That drains a marginal Treasury bid. Nothing about that is priced.

Watch Signal

Watch dollar-yen through the US session. Katayama has spoken. The next step is direct intervention. If it arrives, the Nikkei drop and US chip pain start feeding each other. That correlation becomes reflexive.

The yen at multi-decade lows is not a Japan story. It is a Treasury demand story.

Japanese life insurers are the marginal buyer of long-duration US paper. They fund those purchases with cheap yen. When the yen falls this far, the hedged return on a Treasury flips negative. When the BOJ hikes to defend the yen, JGB yields rise. The same insurers get a return at home. That is when the flow stops.

The Nikkei fell hard overnight. SoftBank led. Those are the visible losses. A yen crisis hits the marginal bid for the ten-year note. That is the quiet loss.

Every arrow today points at less demand for US paper. AI chip pain in Tokyo. Yen at multi-decade lows. Fed centrists opening the door to a hike. Japanese life insurers on watch.

The Read

If dollar-yen breaks past the intervention line, the BOJ meets it with policy. The US long end loses a leg of demand. The Fed meeting is two-sided. The rate-cut trade for the second half narrows into that fork.

This AI Stat Will Shock You

But one little-known statistic suggests the entire sector could be on the verge of a massive collapse.

Warren Buffett once called it “the best single measure of valuations.”

Today, that indicator is flashing far above where it stood before the Dot-Com crash.

If this signal proves right, many AI favorites could fall hard.

See the warning sign and what investors should consider doing now.

Economic Data: Housing Starts and Building Permits (June, 8:30 AM ET), Industrial Production and Capacity Utilization (June, 9:15 AM ET), University of Michigan Consumer Sentiment preliminary reading (July, 10:00 AM ET)

Fed Speakers: None scheduled today. Vice Chair Jefferson spoke Thursday evening.

Earnings: Travelers (TRV), Truist Financial (TFC), Fifth Third Bancorp (FITB)

Overnight: Nikkei -4.03%, Shanghai Composite -3.05%, FTSE -0.27%, DAX -0.71%

Netflix reported.

The market treated it as cover for selling. That was a global AI trade under repricing. Netflix handed the market a reason.

The next fork lands July 29. If Jefferson speaks for the committee, hold is not the base case anymore. If he does not, chip pain already priced a move that will not happen.

Between now and then, the yen decides if this is Japan or global. Watch the intervention line. Watch the Treasury auctions.

The two largest marginal Treasury buyers are getting more expensive together. Japanese life insurers on one side. Chinese reserves on the other.